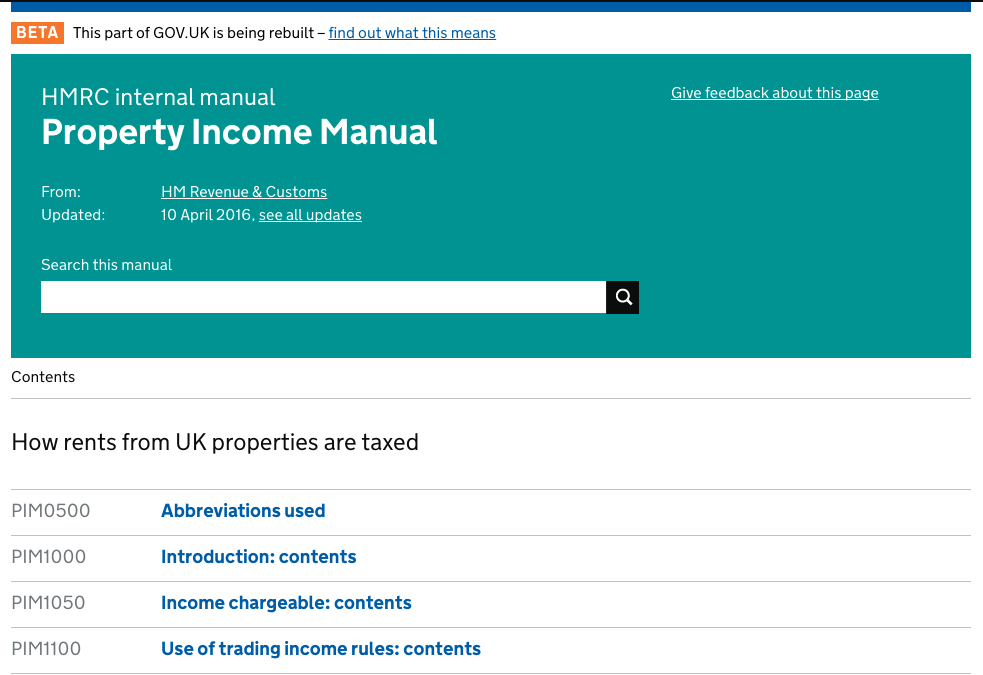

Intm153150 International Manual Hmrc Internal Manual Gov Uk

Intm153150 International Manual Hmrc Internal Manual Gov Uk - These pages form part of the international manual. Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. They contain guidance prepared for hmrc staff and are published in accordance with the.

Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,. These pages form part of the international manual. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements They contain guidance prepared for hmrc staff and are published in accordance with the. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services.

They contain guidance prepared for hmrc staff and are published in accordance with the. These pages form part of the international manual. If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,.

What are M1, N1 & N2 Categories? Clarks Vehicle Conversions

These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. They contain guidance prepared for hmrc staff and are published in accordance with the. We’d like.

Hidden Tax Help For Landlords On The HMRC Web Site Guild of

These pages form part of the international manual. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country.

SELF ASSESSMENT MANUAL PPT

Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. If a.

SELF ASSESSMENT MANUAL PPT

We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign.

Fillable Online capturing a new claim (Info) HMRC internal manual

They contain guidance prepared for hmrc staff and are published in accordance with the. Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,. These pages form part of the international manual. If a customer requires hmrc to certify that they are a resident of.

SELF ASSESSMENT MANUAL PPT

We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements These pages form part of the international manual. Gains from the disposal of ships or aircraft operated in international traffic can only be taxed.

INTM860750 Employees of International Organisations Where exemption

These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements If a customer requires hmrc to certify that.

VAT Business/NonBusiness Manual HMRC Internal Guidance for VAT

We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements These pages form part of the international manual. International tax issues including the principles of double taxation relief and an introduction to double taxation.

SELF ASSESSMENT MANUAL PPT

If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. They contain guidance prepared for hmrc staff and are published in accordance with the. These pages form part of the international manual. International tax issues including the principles of double taxation relief.

Trusts, Settlements and Estates Manual Glossary HMRC Internal

If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,. They contain guidance prepared for hmrc staff and are published in accordance with the. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements. International.

They Contain Guidance Prepared For Hmrc Staff And Are Published In Accordance With The.

International tax issues including the principles of double taxation relief and an introduction to double taxation agreements We’d like to set additional cookies to understand how you use gov.uk, remember your settings and improve government services. These are designed to help businesses understand hmrc’s expectations as they plan, implement, manage, and document. International tax issues including the principles of double taxation relief and an introduction to double taxation agreements.

These Pages Form Part Of The International Manual.

Gains from the disposal of ships or aircraft operated in international traffic can only be taxed in the country where the operator is resident (or,. If a customer requires hmrc to certify that they are a resident of the uk for any purpose other than claiming relief from foreign taxes under a dta,.